Due Diligence

Due diligence is a continuous process to help enterprises identify risks relating to human rights, labour rights and the environment with a view to ending, preventing or mitigating those risks. Due diligence is an essential element of international responsible business conduct and is a key theme of the internationally endorsed OECD Guidelines for Multinational Enterprises (2023) and the United Nations Guiding Principles (UNGPs). Due diligence is also known as supply chain responsibility.

The OECD Guidelines for MNEs acknowledge and encourage the positive contributions that business can make to economic, environmental and social progress, but also recognise that business activities may result in adverse impacts related to corporate governance, workers, human rights, the environment, bribery, and consumers. Due diligence is the process enterprises should carry out to identify, prevent, mitigate and account for how they address these actual and potential adverse impacts in their own operations, their supply chain and other business relationships... The purpose of due diligence is first and foremost to avoid causing or contributing to adverse impacts on people, the environment and society, and to seek to prevent adverse impacts directly linked to operations, products or services through business relationships. When involvement in adverse impacts cannot be avoided, due diligence should enable enterprises to mitigate them, prevent their recurrence and, where relevant, remediate them.

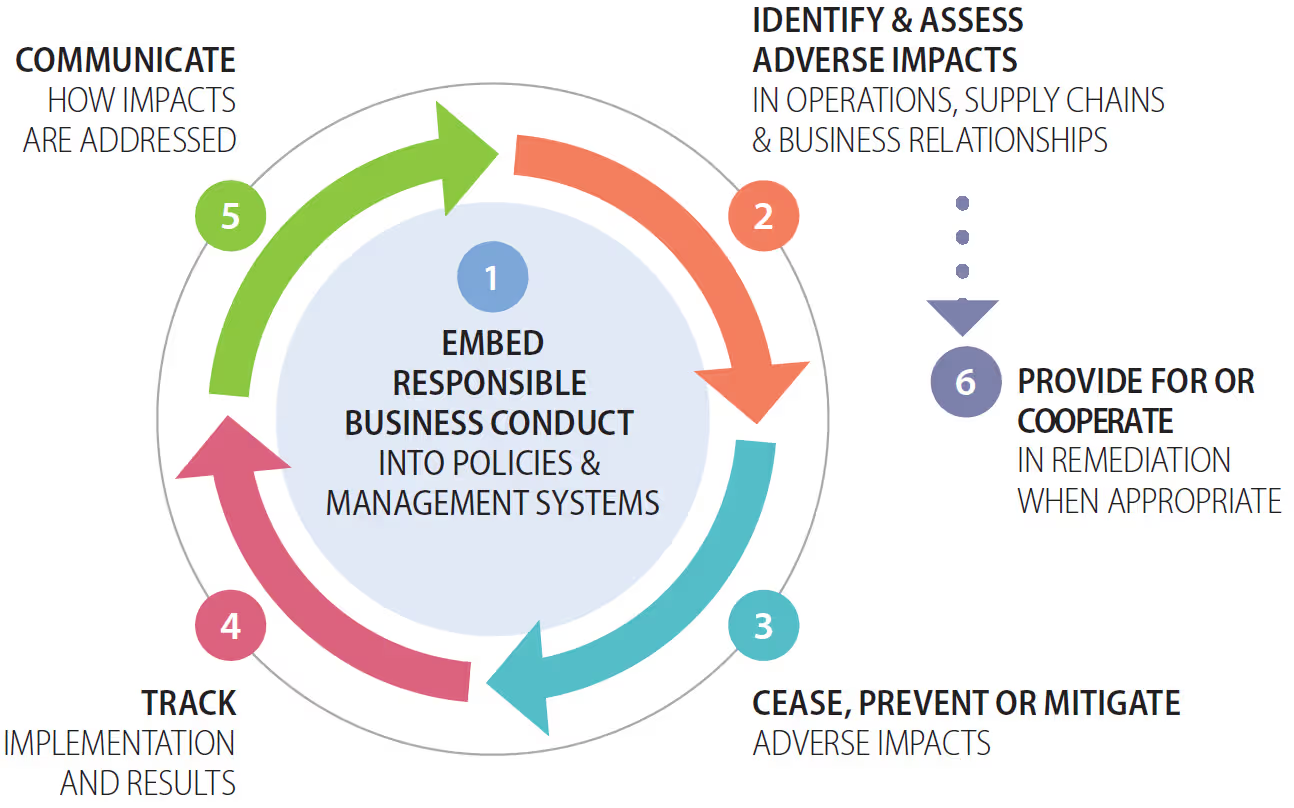

The due diligence process consists of six stages which are explained in the due diligence guidance and flyers. You can find these documents and the OECD guidelines in the navigation bar above.

Written text of the image of the six stages of the due diligence process

The figure is a circle. The circle best be read from the middle of the circle (step 1) to top right (step 2) en then around the clock (step 3 to 6):

- embed responsible business conduct into polities and management sysems;

- identify and assess adverse impacts in operations, supply chains and business relationships;

- cease, prevent or mitigate adverse impacts;

- track implementation and results;

- communicate how impacts are addressed;

- provide for or cooperate in remediation when appropriate.

Due Diligence Guidances per Sector

Besides the generic OECD Due Diligence Guidance, the OECD has also developed the following sectoral Guidances.

- Responsible business conduct in the financial sector;

- Responsible business conduct and technology;

- Responsible Supply Chains in the Garment and Footwear Sector;

- Responsible Agricultural Supply Chains

- Responsible Supply Chains of Minerals;

- Responsible business conduct, environment and climate change.

You can find these sectoral guidances on the OECD website 'Responsible Business Conduct OECD Guidelines for Multinational Enterprises'.